Cross-border payments are getting popular as more and more startups, LLPs, private limited companies, and other SMEs are going international in their dealings. In India, the startup ecosystem has grown by leaps and bounds.

The number of startups in India increased to over 70,000 in June 2022 from only 471 in 2016. The growing number of startups and SMEs, which range from single-handedly run proprietorships to ever-perpetual companies, is one of the reasons that India is the largest receiver of inward remittances globally.

However, every cross-border transaction is subjected to some rules. These rules are set by the central financial institution of a country. For instance, remittances are governed by the Reserve Bank of India (RBI) and the Foreign Exchange Management Act (FEMA) in India.

Whether you are sending money abroad or receiving it from abroad, you must specify the purpose of such cross-border transactions, which we know as purpose codes. Purpose codes are issued by the government of a country to overlook all the transactions happening in and out of the country. These codes also enable the smooth processing of the cross-border payment system.

But what if you choose the wrong purpose code? Do you lose the money? Let's find out.

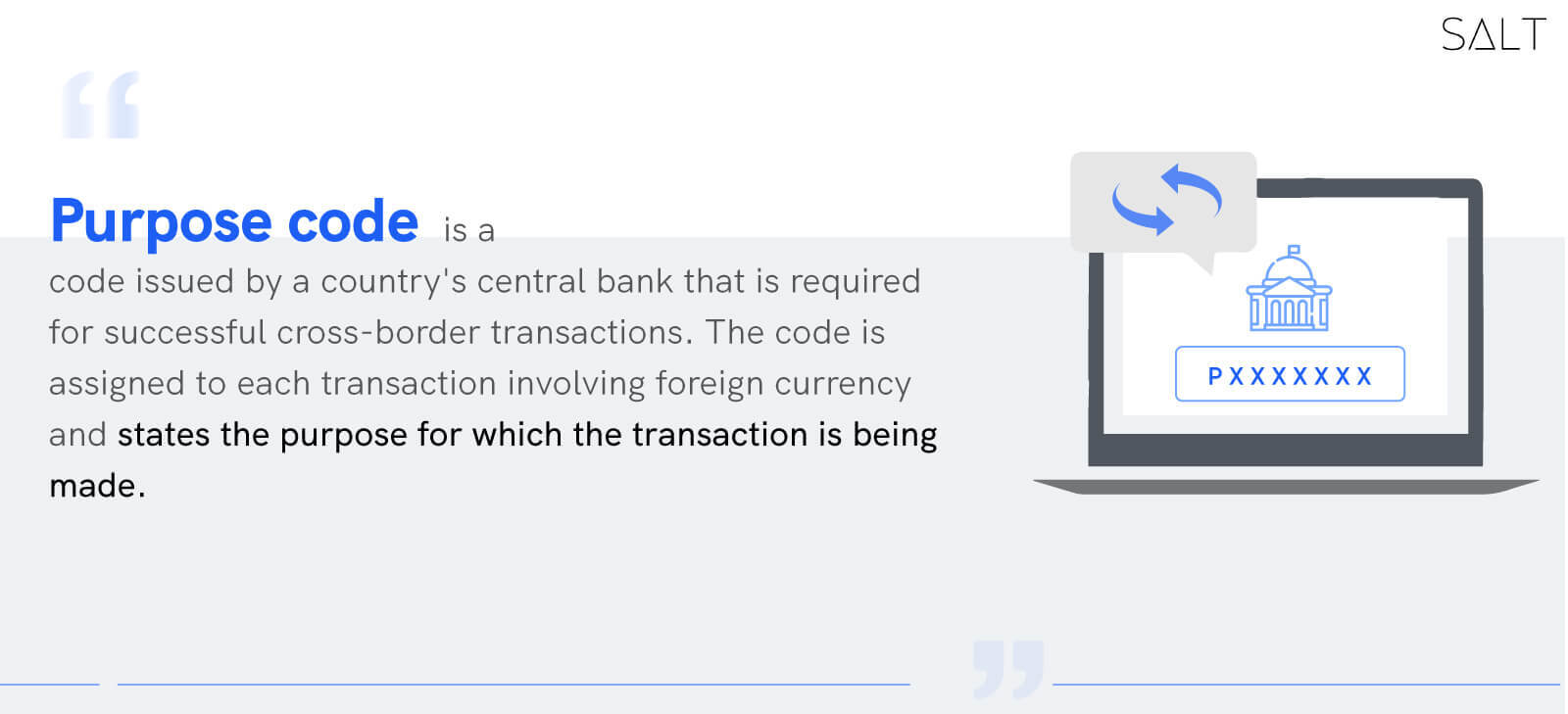

What is the Purpose Code?

Countries around the world issue purpose codes through their central banking institutions. A purpose code is required for cross-border transactions to be successful. Each transaction involving foreign currency is assigned a separate purpose code.

A purpose code specifies the purpose of the transactions, i.e., why the transaction is being performed. When making a cross-border payment, purpose codes from both the sender and receiver countries may be required in order to meet the regulatory requirements of the banks issuing the codes.

In India, RBI has various purpose codes for both payments received by Indians from abroad and payments sent by Indians abroad.

In other words, the purpose code assists regulators in determining the precise nature of a cross-border transaction, whether it is inward remittances in foreign currency or outward remittances in foreign currency.

Why is It Needed?

The RBI has a list of purpose codes that must be included in the details of every remittance. These codes specify the nature of the transaction as well as the specific reason for the transfer. The RBI can classify remittances using these codes. For example, if the purpose of your foreign transaction is 'postal services,' you must use the code P0401 when processing the transfer.

Many startups, freelancers, and SMEs in India use payment gateways such as Salt, PayPal, Wise for both inward and outward remittances. Before you can withdraw funds from your account to your local Indian bank account, you must first select the correct purpose code if you use a payment system to receive payments in foreign currency. It will be used as the default reason for all future payments once you enter the correct purpose code for your remittances. Along with the correct purpose code, you will also need a Foreign Inward Remittance Certificate (FIRC) issued by RBI to receive cross-border payments.

What Happens When You Choose the Wrong Purpose Code?

As stated earlier, purpose codes are required for both inward and outward remittances. If you select the incorrect purpose code, the central bank may flag the transactions as an attempt to evade taxes. Wrong purpose codes can cause your transactions to fail. Furthermore, the bank may suspend the amount on charges of tax evasion and book you under the tax laws of the land. If the transaction involves a larger sum, the risk of losing the money upon selecting the incorrect purpose code increases. If you enter the wrong purpose code, you will be unable to change it for previous transactions.

RBI has issued about 188 purpose codes and it’s always safe to cross-check your purpose code before filling the details. Instead of scouring through the endless list of codes, you can use SALT’s purpose code finder tool.

Watch this YouTube video to understand How to choose a purpose code for your international transfers.

How Does SALT Help in Cross-Border Transactions?

Excessive transaction fees and a lengthy waiting period make cross-border payments difficult. Banks from different countries deal with one another in cross-border transactions. Aside from currency conversion, there are other considerations, such as varying taxable amounts and hidden fees.

Because there are so many entities involved in a single transaction, the process can be quite slow. SALT, on the other hand, makes cross-border payments easier than ever for all kinds of B2B processes.

SALT is a neobank that works hard to make cross-border payments simple for businesses. SALT allows you to transfer money from abroad in 24 hours for a low fee of only 1.75% of the total transaction amount.

Furthermore, unlike traditional financial institutions, the SALT verification process is simple and quick. You simply need to register on SALT and fill out the necessary information from the comfort of your own home.

SALT does not require a minimum transaction amount to use its services, whether you are a startup, an LLP, a private limited company, or an SME.

There are no hidden fees, annual subscription fees, or markup fees when you use SALT. As a result, with SALT, any business or even a large corporation can easily perform cross-border payments across the globe.