You need information if you intend to send money abroad. You may find all the answers you need regarding tax remittance.

There’s likely to be many reasons you may need to send cross-border payments to India from abroad. But is sending them funds through international money transfers acceptable legally? How much money can you send in the form of inward remittances? What's more, will you or they be subjected to any financial obligations in the form of taxes?

Contents

- How Do Foreign Inward Remittance Get Taxed In India?

- What factors might affect whether your money transfer is taxed?

- Money transferred: Does your transfer amount surpass the country's tax threshold?

- When is the money sent to someone in India from a foreign country taxable?

- How much money can be sent as inward remittance to India annually for personal purposes?

- What kind of tax may be charged on inward remittances?

- Tax for sending money from the USA to India

- Tax for sending money from the UK to India

- RDA, MTSS, and differences between the two

- Transfer Charge

- FAQs

Here is everything you need to know about the regulations in India governing inward remittances.

How Do Foreign Inward Remittance Get Taxed In India?

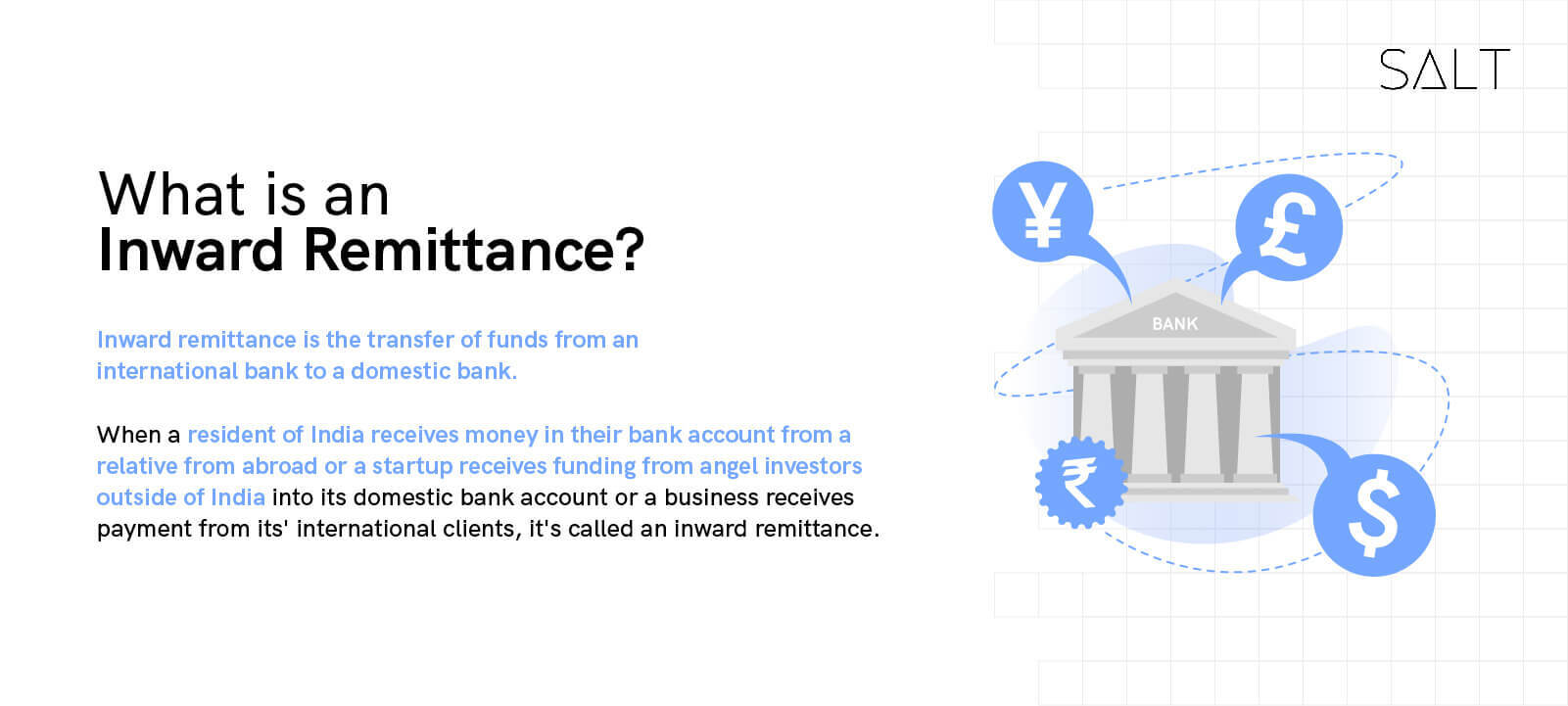

The money one receives in an Indian bank account from abroad is called an inward remittance, and foreign inward remittances come under the governance of the FEMA or the Foreign Exchange Management Act. Foreign inward remittances will be tax-free in the following cases:

- If it is living expenses or financial support for someone

- If the inward remittance is a gift

- If it is for educational purposes

- If the inward remittance is being sent for medical treatment

- If the money is for travel expenses, investments, or donations

Notably, the FEMA also specifies which family members can receive tax-free inward remittances in India

- The sender’s legal spouse

- The sender’s siblings

- The siblings of the sender’s spouse

- The siblings of the sender’s parents

- Any of the legally accepted lineal ascendants or descendants of the sender

- Any of the legally accepted lineal ascendants or descendants of the sender’s spouse

- Any spouses of people belonging to the above categories

If the inward remittance is sent to anyone other than these mentioned relatives, it will be taxed by the government as income if it goes above 50,000 rupees annually.

Further, there are inward remittances under Business payments received in India. Of course, any income earned as Business income, say in the form of consultancy service, is taxed in India. Business payments regarding good receipts are taxed post-deduction of all expenses.

Personal inward remittances to India are permitted under the MTSS, including remittances for family support and remittances to foreign tourists visiting India from their families and friends overseas. Other types of remittances are not permitted, like contributions to nonprofit organizations, trade-related remittances, remittances for investments, or credit to NRE (Non-Residents External Accounts).

A family is only permitted to receive 30 remittances and $2,500 in one calendar year.

The Overseas Principal, or foreign money transfer companies, handle the financial transactions for the MTSS, while Indian agents deliver the money to India's beneficiaries at the current exchange rates.

Rate of TCS on foreign remittance

The current Income Tax regulations have specified rates for TCS collection on international remittance under the LRS. If a buyer presents a PAN card, TCS will be deducted 5% from any sum sent outside for any purpose under the plan; otherwise, the tax would be applied at 10% with a transaction amount threshold of INR 7 Lakhs. However, tax is deducted at source at a rate of 0.5% on any funds transferred to repay a loan obtained from a bank to pay for education again with a threshold of the transaction amount of INR 7 Lakhs. Rates of TDS is 5% if the loan is ‘not’ taken from financial institution. FurtherAgain, the TCS rate applied to the transaction is 5% if the person cannot present their PAN card.

Then there is the selling of international travel packages, where the purchaser is subject to either a 5% source tax or a 10% source tax. In contrast to the LRS, there is no minimum exemption threshold for the amount when a tour package is sold.

Budget 2023 has changed the above rates. Currently, the TCS rate is raised from 5% to 20% on all remittances under LRS scheme on all remittance except education purposes with no threshold limits at all. Remittances for the purpose of education continues to be at 0.5% if taken from financial instution, 5% if taken from other sources. Incase PAN is not there, 20% becomes 40%, 0.5% becomes 5% and 5% changes to 10%.

It is pertinent to note that these are not taxes collected at source and the person can claim a refund if returns are duly filed.

Further, there is no limit on the amount of inward remittance made in case of business receipts.

What factors might affect whether your money transfer is taxed?

Even if not all money transfers are taxed, it's still vital to be aware of the situations in which you may need to file a tax return and pay taxes to comply with the law. Of course, these elements can all vary based on your location and the recipient's location.

The funds' source:

Are they coming from a pension, the sale of a residence abroad, or an inheritance fund? The source can significantly impact whether your money transfer is subject to tax.

The two nations' tax regulations:

Different nations have different tax laws, including rules on how much must be reported to the appropriate tax authorities and regulatory agencies to prove the funds were obtained legitimately.

Money transferred: Does your transfer amount surpass the country's tax threshold?

In the case of Business payments, the same is governed by the laws of both countries. One must be vigilant of certain reportings in other jurisdictions, if applicable. In Inward remittance of a business nature, FIRC/FIRS must be obtained as proof of receipt.

When is the money sent to someone in India from a foreign country taxable?

While there is no cap on the amount of money, you can send to your family, the nation you’re sending to may have regulations and restrictions on the highest amount you can send to India without being subject to tax. After a certain threshold, your sending country may start taxing money sent outside.

How much money can be sent as inward remittance to India annually for personal purposes?

The amount of money you can send to your parents in India without taxation has no upper limit.

Any money sent as a gift to any qualifying relative listed in the FEMA regulations is thought to be tax-free. However, suppose money is transferred to someone not on the list. In that case, they are regarded as non-relatives, and if the amount received exceeds Rs 50,000 in a year, it will be taxed as income.

What kind of tax may be charged on inward remittances?

Individuals in India can receive an inward remittance in either a rupee drawing arrangement (RDA) or a money transfer service scheme (MTSS). Under the RDA, there is no limit on how much money can be sent overseas for personal purposes. Under MTSS, each inward remittance is restricted to $2500.

Different fees apply to inward transfers. The price is determined by many variables, including the current exchange rate, correspondent bank fees, type of transfer, account type, and country of origin. The projected costs will be disclosed to you by your bank before the transaction is finalized.

Similarly, Business payments can be received under OPGSP or SWIFT. A limit of $10,000 per transaction under OPGSP is usually used for smaller trade payments. SWIFT is used for larger payments, and it is moved through a financial institution. The cost associated with OPGSP is the conversion charges and issuance of FIRC charges. Cost with SWIFT can be SWIFT charges, Conversion Charges, Correspondent bank fees or any other charges depending upon the financial institution.

Tax for sending money from the USA to India

According to the IRS, if you live in the US and wish to send money as a gift to family members in India, you can do so up to $15,000 every year without paying taxes on the transfer. However, most gifts over USD 15,000 will result in a tax event.

Tax for sending money from the UK to India

Under the yearly exemption, you can send gifts worth up to £3,000 to the UK during the fiscal year. Additionally, you are permitted to present gifts for weddings or civil ceremonies of up to £1,000 per person, £5,000 for children, and £2,500 for grandchildren or great-grandchildren.

RDA, MTSS, and differences between the two

According to the Reserve Bank of India, there are two ways to receive inward remittances to India from the UK abroad: RDA and MTSS.

RDA is typically only permitted for private accounts. Money transfers can also be made for business purposes up to a specific amount. The RDA does not allow cross-border money transfers from India to other countries; but permits remittances into India exclusively.

Personal remittances to India are permitted under the MTSS, including remittances for family support and remittances to foreign tourists visiting India from their families and friends overseas. However, any other type of remittance, such as contributions to charitable trusts, remittances connected to trade, or remittances for purchasing real estate, is prohibited.

Transfer Charge

You should check with the bank for the fees associated with sending money overseas to your parents' bank account. Before the transaction is completed, the bank will let you know about the transfer fees. The price is determined by several variables, including the current exchange rate, the bank's fees, the nation from which the remittance is being made, the type of transfer, and the type of account, among others.

Conclusion

In a nutshell, it depends. The amount you receive (large sums are more likely to be classified as income or gifts that may be taxable), the reason you're receiving the money (is it a foreign inheritance, a remittance payment from a family member abroad?), and the specific tax laws in your own country will all determine whether your international money transfer is taxable.

FAQs

For what reasons can you send money?

You can send money for visits abroad (aside from Nepal and Bhutan), gifts, donations, employment, emigration, maintaining close relatives, business travel, attending conferences or specialized training, medical expenses or check-ups, or for going with a patient for treatment or a check-up; studies abroad; or any other current account transaction that isn't covered by the definition of the current account in FEMA 1999.

What documents are needed?

You must submit the A2 cum LRS declaration form, identification and address proofs, and Permanent Account Number (PAN). You might also be required to submit particular documents, such as a passport, visa, ticket, invoices from the travel agency, or anything else the bank or transferring agency requests, depending on the purpose of the remittance. You must also provide Form 15CA and, in some situations, Form 15CB, a certificate from a chartered accountant proving the tax paid if you send money to a non-resident individual or a foreign business.

How long will it take?

The transfer can happen immediately or take up to 30 days, depending on your payment method.

How may the funds be transferred?

Both online and offline methods of sending money are commonly provided by banks and private money transfer and exchange firms.

Watch this youtube video on How is inward remittance taxed in India.